The Bill Comes Due

How the AI infrastructure boom is being built on economic sand, and what that means for the communities asked to absorb its costs

For three years, the hyperscale data center industry has operated on projections. Demand forecasts, adoption curves, and revenue models built on assumptions about how deeply artificial intelligence would embed itself into corporate life. Communities across the Sun Belt, including right here in Southern Arizona, have been asked to extend water allocations, accommodate grid load, approve permitting exceptions, and absorb fiscal risk based entirely on those projections.

Last week, for the first time, we got financials.

The SpaceX S-1 IPO prospectus, filed in May 2026, contains the most detailed public accounting yet of a frontier AI company’s economics. The subject is xAI, Elon Musk’s artificial intelligence division, which SpaceX absorbed in a February 2026 merger. What the filing reveals is not a growth story. It is a loss ledger; accelerating losses, escalating debt, and a capital burn rate that one analyst characterized as either the most rational bet in technology history or the setup for the largest venture-funded correction the world has ever seen.

This report uses the xAI disclosure as a lens. It connects those numbers to the broader enterprise adoption picture now emerging, Fortune 500 companies hitting budget walls after four months, token-based pricing making AI more expensive than the employees it was supposed to replace, and a growing body of academic research showing that after hundreds of billions in capital deployed, AI has added, by the chief economist of Goldman Sachs’s own accounting, “basically zero” to U.S. GDP.

The infrastructure being built on that economic foundation includes facilities planned and already operating in Marana, Tucson, and similar communities across the American Southwest. The communities are not party to the bet; they are the collateral.

What the SpaceX S-1 Reveals

The SpaceX IPO prospectus is a 277-page document. Most of the media coverage focused on the rocket company’s impressive Starlink satellite business, which is genuinely profitable and interesting, but buried in the segment financials is the first hard look anyone outside xAI’s investor circle has had at what it actually costs to build and run a frontier AI model company.

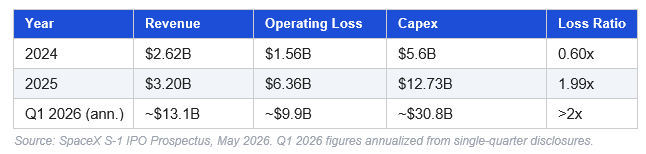

In 2024, xAI recorded a $1.56 billion loss on $2.62 billion in revenue. By 2025, losses had expanded to $6.36 billion on $3.20 billion in revenue. The company was spending approximately two dollars for every dollar it collected, and rather than narrowing, the gap is widening.

The capital expenditure trajectory is particularly important for understanding the data center buildout picture. xAI spent $12.73 billion on infrastructure in 2025, 61% of all SpaceX capex that year. In the first quarter of 2026 alone, it spent $7.7 billion, bringing the annualized run rate to approximately $30.8 billion. In a single quarter, xAI’s share of SpaceX’s capital expenditure climbed to 76%.

To put that in perspective: xAI’s 2025 capex by itself exceeded the combined capital spending of SpaceX’s Starlink and rocket launch divisions. The profitable, cash-generative satellite internet business is being outspent by its money-losing AI sibling by more than 3x.

“If you compare xAI to a traditional SaaS company, the financials look reckless. If the payoff happens, the $1B+ per month burn will be viewed as a bargain. If it doesn’t, we are looking at the largest venture-funded correction in history.” — Harrison Rolfes, Senior Research Analyst, PitchBook

To fund this pace of spending, xAI borrowed aggressively. The company took on $16 billion in new debt in 2025 alone to finance its GPU buildout. When SpaceX absorbed xAI in February 2026, it took out a $20 billion bridge loan and used the proceeds to pay off xAI’s debt stack, effectively refinancing the AI division’s losses onto the rocket company’s balance sheet, using Starlink’s profitability as the backstop.

The world’s most profitable satellite internet business is now the financial guarantor of an AI division losing money at an accelerating rate. SpaceX’s total liabilities reached $60.5 billion as of Q1 2026, largely driven by the xAI merger, while cash reserves declined from $25 billion to $16 billion in a single quarter.

Investors approaching the SpaceX IPO, targeting a $1.75 trillion valuation, are being asked to pay for Starlink’s genuine performance and xAI’s speculative bet in the same package. The S-1 itself states that the $2 trillion target assumes roughly $1 trillion in value from businesses that are currently unprofitable.

Who Is Building What, and on What Assumptions

xAI is not an outlier; it is the only frontier AI company with publicly available financials. That distinction matters enormously because it means xAI’s numbers are the first data point, not an average, or a representative sample, in a category that includes OpenAI, Anthropic, Google DeepMind, Meta AI, and Amazon’s Bedrock infrastructure.

OpenAI and Anthropic are reportedly planning IPOs as early as Q3 2026, looking to public markets to fund capital requirements they cannot sustain privately. OpenAI is targeting a valuation of $750 billion to $830 billion. Anthropic, despite having recently signed a term sheet at a $900 billion valuation, reportedly expects its first operating profit in Q2 2026, though on the back of a 130% revenue jump, which raises its own sustainability questions about the pace of growth required to justify the valuation.

These companies are not operating in a vacuum, they are the demand signal for the hyperscale infrastructure buildout. Alphabet, Amazon, Microsoft, and Meta announced plans to invest over $350 billion in data center infrastructure in 2025, rising to approximately $400 billion in 2026. The global data center sector is projected to require up to $3 trillion in investment by 2030, growing at a 14% compound annual rate.

The investment thesis runs as follows: AI model companies will grow into their losses as enterprise adoption scales. Scaled adoption will drive compute demand. Compute demand will fill the data centers. The data centers will service the debt. It is a chain of dependencies, each link contingent on the one before it.

A Moody’s report in mid-2025 warned that the AI-driven data center boom raised heightened credit and overbuild risks, highlighting the shift to gigawatt-scale ‘AI factory’ campuses and noting that without disciplined power sourcing and risk-sharing structures, the boom risks tipping into credit stress. The report noted the key bottleneck: the computing needs that data centers will serve in the future remain uncertain, given the constant flow of technological breakthroughs, making long-term credit risk assessment exceptionally difficult.

“History has shown that even high-tech real estate is not immune to cycles. Prudent investors will remember the telecom and data center glut of the early 2000s.” — MMCG Investment Research, March 2026

The telecom parallel is instructive. In the late 1990s, fiber optic cable was laid on an enormous scale in anticipation of internet traffic that was genuinely coming, but not on the timeline the capital structure required. The infrastructure and demand were real, but the timing mismatch was catastrophic. Data centers were abandoned. Debt was restructured. Communities that had welcomed the buildout were left with stranded assets and broken fiscal promises.

The current buildout has one structural difference that makes the risk argument slightly more nuanced: much of the new capacity is pre-leased to hyperscalers rather than speculative. Roughly 73% of projects under construction as of mid-2025 were already committed to Microsoft, Google, Amazon, or Meta. But that structure introduces its own risk, counterparty concentration. The market is not liquid. There are no alternative buyers at scale. When it is time to sell or refinance, the only buyers are the hyperscalers themselves, who have every incentive to wait for distressed pricing. If one or two of those hyperscalers pulls back its build commitments, as Microsoft has already begun to do in specific markets, the domino effect on speculative secondary-market capacity could be substantial.

When Usage Costs More Than Humans

The infrastructure investment thesis depends on enterprise demand absorbing the capacity being built. That demand is measured in token consumption, the metered usage of AI models that generates revenue for the labs and load for the data centers. In 2025 and early 2026, two of the most sophisticated technology consumers in the world ran a real-world experiment to determine what enterprise-scale token consumption actually costs, and the results were not what the projections anticipated.

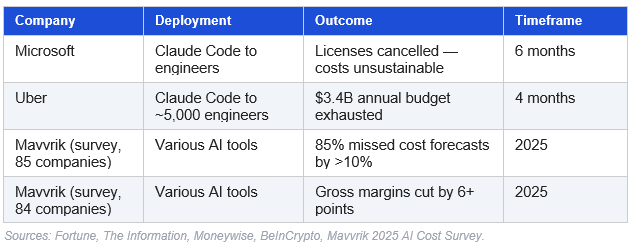

In December 2025, Microsoft deployed Anthropic’s Claude Code agentic coding tool to thousands of its engineers across the Experiences and Devices division. Adoption was rapid and deep; by early 2026, engineers were using it for code generation, debugging, and review at rates exceeding those of any prior software tool rollout.

In mid-May 2026, Microsoft began winding down those licenses. Access for the division ends June 30, 2026, six months after launch. The tool was not canceled because engineers disliked it; it was canceled because they used it too much. Token-based billing had made consumption unsustainable at the deployment scale. Engineers were directed to use Microsoft’s internal Copilot CLI tool instead.

Uber’s experience creates a concrete confirmation of the experience. The company deployed Claude Code to approximately 5,000 engineers in December 2025. By April 2026, adoption had reached 84% of the engineering organization, with 70% of committed code originating from AI tools. Per-engineer monthly costs ranged from $500 to $2,000. Uber’s Chief Technology Officer, Praveen Neppalli Naga, made the situation public: the company had burned through its entire $3.4 billion 2026 AI budget in four months.

“I’m back to the drawing board, because the budget I thought I would need is blown away already.” — Praveen Neppalli Naga, CTO, Uber, April 2026

Uber’s operations chief, Andrew Macdonald, added a more fundamental concern: token usage did not seem to correlate directly with useful consumer features. The company was spending at a rate that would exhaust three times the annual budget before year’s end, and the value of the output was difficult to trace to business results.

These are not small companies with unsophisticated procurement operations. Microsoft and Uber are among the most technologically capable enterprises in the world. If they cannot forecast or control AI tool costs at deployment scale, the enterprise adoption curve that underpins the infrastructure investment thesis is far less certain than the projections suggest.

The structural dynamic that explains why costs are difficult to control is that agentic AI tools consume dramatically more tokens per task than standard models. Gartner’s analysis found that while token prices are falling at the commodity level, agentic systems, which chain together multiple model calls, tool uses, and reasoning steps, drive consumption far higher per unit of work. Gartner’s conclusion: chief product officers should not confuse the deflation of commodity tokens with the democratization of frontier reasoning. Cheaper inputs do not guarantee cheaper outputs when the number of inputs per task is multiplying.

The broader market is reacting accordingly. GitHub, responding to enterprise budget pressure, announced a shift to usage-based billing for all Copilot plans through GitHub AI Credits starting June 1, 2026, a move that transfers consumption risk directly to customers. AI software prices across the U.S. have climbed 20-37%. The economics of widespread deployment are proving stubbornly resistant to the cost curves the industry projected.

The Productivity Mirage

The enterprise cost crisis would be less significant if the productivity gains were commensurate and organizations were seeing output improvements that justified the spend. The academic and economic research record suggests they are not.

The most direct evidence comes from a National Bureau of Economic Research study published in early 2026. Researchers surveyed nearly 6,000 senior executives, CEOs, CFOs, and equivalents across the United States, the United Kingdom, Germany, and Australia. Among their findings: approximately 70% of firms reported using AI. Of those, 90% said it had produced no measurable impact on productivity or employment. Senior executives using AI themselves averaged 1.5 hours per week of engagement.

This is not the picture of transformative technology embedded in enterprise operations. It is a picture of widespread, shallow adoption, tools installed and used only occasionally, without the workflow restructuring and organizational change required to generate the productivity gains that would justify infrastructure investment.

“70% of firms report using AI, yet 90% say it has had no measurable impact on productivity or employment so far.” — National Bureau of Economic Research, February 2026

Goldman Sachs Chief Economist Jan Hatzius was direct about the macroeconomic implications. Speaking with the Atlantic Council, he stated that all the major AI investments of 2025 had generated “basically zero” contributions to U.S. GDP growth. His explanation is important for the Southern Arizona context specifically: a substantial portion of AI investment flows directly to Taiwan (TSMC) and South Korea (Samsung, SK Hynix) for chips. That spending adds to Taiwanese and Korean GDP, not to American GDP. The infrastructure spending that does occur domestically, the data centers, the power infrastructure, and the land generate construction employment, but the economic return on the compute investment itself has not materialized in measurable output.

The Penn Wharton Budget Model’s long-range forecast provides useful calibration. Even under optimistic assumptions about adoption and diffusion, the model estimates AI will increase U.S. productivity and GDP by 1.5% by 2035, nearly a decade from now. The annual boost to productivity growth is projected to eventually fade to a permanent effect of less than 0.04 percentage points, against a capital commitment running into trillions of dollars. This is a modest return on an extraordinary investment, and it is the optimistic projection.

ManpowerGroup’s 2026 Global Talent Barometer, surveying nearly 14,000 workers across 19 countries, found that regular AI use increased by 13% in 2025, while confidence in the technology’s utility fell by 18%. Workers are using the tools more but trusting them less. The diffusion pattern is not deepening into the kind of workflow integration that drives productivity gains; it is broadening at the surface while remaining shallow beneath the surface.

A parallel OECD survey found that among small and medium-sized enterprises that had adopted generative AI, 83% reported no change in staffing levels, not because AI was augmenting human productivity, but because it was not changing operations enough to affect headcount decisions at all. The largest barrier cited by non-adopters is the lack of suitability for their work (57%). Not cost. Not access. Suitability.

This matters for the investment thesis because the infrastructure buildout assumes a fundamentally different trajectory: AI will become essential infrastructure for a broad range of business processes, driving sustained, growing compute demand for decades. If the productivity research suggests that AI’s impact is real but concentrated in specific domains, and shallow outside them, the total addressable market for sustained enterprise compute consumption may be substantially smaller than the data center construction pipeline assumes.

What This Means for Southern Arizona

The hyperscale data center buildout in Marana, the broader Tucson metropolitan area, and the Sun Belt corridor is not funded by proven revenue streams; it is funded by capital markets extending credit against a consumption future, as leading enterprises, such as Microsoft, Uber, and dozens of others, quietly adjust their AI budgets, which they cannot currently sustain at scale. The academic record suggests that the productivity gains used to validate the long-range demand projections have not materialized in measurable terms, and the only public financial disclosure from a frontier AI company shows accelerating losses rather than converging toward profitability that would make the bet sensible.

Communities absorbing the cost of this buildout, the water draw, the grid load, the air quality burden, the fiscal infrastructure, are not party to the bet. They are told they are receiving economic development. What they are actually receiving is exposure to the downside of a capital markets wager they did not make and cannot unwind.

The specific risks for Southern Arizona deserve naming:

Water. The Project Blue complex and similar facilities represent significant, long-term commitments to consumptive water use in one of the most water-stressed regions of North America. That commitment is justified on the basis of operational demand, how much computing the facilities will run, and for how long. If the enterprise demand that drives that compute does not materialize on the projected timeline, the water commitment does not automatically recede. The infrastructure is built. The draw continues.

Grid load. Data centers now consume a disproportionate share of Arizona’s grid capacity, with implications for rate structures and reliability for residential and commercial customers who are not the primary beneficiaries. The IEA projects global data center electricity consumption will reach 600 terawatt-hours in 2026, a 14% increase from 2025, which was itself a 20% increase from 2024. The doubling of grid burden over two years is an infrastructure reality regardless of whether AI revenue projections are met.

Fiscal risk. The tax increment financing, water infrastructure extensions, permitting accommodations, and utility concessions associated with hyperscale development are justified by projected fiscal returns: employment, property tax, and ancillary economic activity. The telecom infrastructure buildout of the late 1990s produced stranded assets, broken economic development promises, and restructured debt at high local cost. The data center concentration of the 2020s has structural similarities that deserve scrutiny before the community commitments are locked in for decades.

The communities absorbing the water draw, the grid load, the air-quality burden, and the fiscal risk are not parties to the bet. They are the collateral.

The SpaceX S-1 filing changes the evidentiary landscape. For the first time, policymakers, community advocates, and regulators have a public document, subject to SEC disclosure standards, that quantifies what the AI infrastructure bet actually costs per unit of revenue generated. When a company approaches a municipality with demand projections that justify significant public accommodation, that document now exists as a reference point.

The question it enables is simple: if the most visible frontier AI company, after multiple years of operation and tens of billions in capital deployment, is losing money at an accelerating rate while its largest enterprise customers are hitting budget walls after four months of deployment, on what basis are the 15-year demand projections underlying this facility’s design load calculated?

That is not an anti-development argument; it is a due diligence question. Communities have both the right and the responsibility to ask it.

What to Watch

The SpaceX IPO roadshow begins June 8, 2026. The institutional investor reception, particularly how analysts price the xAI segment relative to the Starlink segment, will be an important early signal about whether the market is beginning to discount the AI infrastructure bet more rigorously.

OpenAI and Anthropic are planning their own public offerings, potentially as early as Q3 2026. Those filings, if they proceed, will provide additional financial disclosure for the first time. The picture may be better than xAI’s, or it may confirm a pattern.

In the interim, the enterprise adoption data will continue to accumulate. Token economics will either stabilize to make deployment cost-effective at scale, or budget overruns at Microsoft, Uber, and their peers will deepen. The productivity research will either begin to show the J-curve inflection that technology economists expect from general-purpose technologies, or it will not.

The Sonoran Think Tank will continue tracking all of it, with the same tools we bring to every policy question in this region: primary sources, quantitative framing, and a commitment to the communities that live with the consequences of decisions made in boardrooms and capital markets far from here.

SOURCES CITED IN THIS ANALYSIS

SpaceX S-1 IPO Registration Statement, filed May 2026 (SEC EDGAR)

Morningstar / PitchBook: “Financials Look Reckless: Lifting xAI’s Hood in the SpaceX IPO,” May 2026

TechCrunch: “xAI burned $6.4B last year — SpaceX’s IPO filing shows why the spending is far from over,” May 2026

Fortune: “Microsoft reports are exposing AI’s real cost problem,” May 2026

The Information / Moneywise: Uber CTO budget exhaustion reporting, April 2026

Futurism / Goldman Sachs (Jan Hatzius, Atlantic Council interview): AI GDP contribution analysis, March 2026

National Bureau of Economic Research: “Firm Data on AI” working paper, February 2026

Penn Wharton Budget Model: “The Projected Impact of Generative AI on Future Productivity Growth,” September 2025

Moody’s: “Data Centers: Managing Risk Amid a Market Boom,” January 2026

MMCG Investment Research: “U.S. Hyperscale Data Center Development,” March 2026

ManpowerGroup Global Talent Barometer 2026; OECD SME AI Adoption Survey 2025

JLL 2026 Global Data Center Market Outlook; IEA Global Energy and AI 2026

Mavvrik 2025 AI Cost Survey; Tom’s Hardware / Goldman Sachs token economy analysis, May 2026

Sonoran Think Tank (STT) is a Southern Arizona civic research organization. All STT content is published free and open to the public. No paid subscription tier. Analyst voice, not advocacy.

Good to know! Thanks